New Look has lost brand appeal having failed to remain relevant among its core UK shopper base, with product and its store environment in particular lacking differentiation in an increasingly competitive market. This contributed to an 8.4% decline in UK like-for-like sales in H1 FY2017/18, and has led to crisis speculation in 2018 with rumours of store closures and a company voluntary arrangement (CVA).

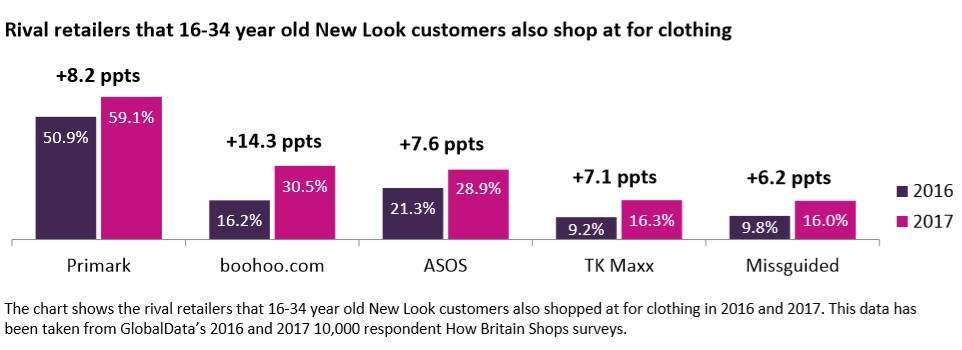

New Look has unsuccessfully reacted to the rise of online pureplays ASOS, boohoo.com and Missguided as well as value rival Primark. Subsequently, its share of the UK clothing market is forecast to decline 0.3 percentage points to 2.2% between 2016 and 2018. Despite sitting on debt of more than £1.1bn, capital expenditure is crucial to protect it from slipping out of the top 15 UK clothing retailers in 2018 – this time last year New Look ranked 10th.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Investment in product must be a top priority. While New Look’s proposition provides value in its mix of trend-led and basic pieces, it has not kept up with the online pureplays which offer a greater range of fast fashion and more boundary-pushing designs to draw in the 16-24 year old shopper. New Look’s product range is safer and lacks excitement in comparison, particularly in its smaller stores, which has led to customer erosion and increased levels of shopping around among its customer base.

With the younger end of the market more saturated, it would be tricky for New Look to win back lapsed tween and teen customers. Therefore, it must consider narrowing its target shopper base by improving appeal among 25-34 year old value-driven consumers that have become dissatisfied with the current high street offer – stealing shoppers from the likes of Next, Debenhams and Dorothy Perkins. Quick reaction and translation of seasonal trends is still vital, but by targeting a slightly older core audience to the online pureplays it will allow New Look to differentiate its product ranges and make them more relevant to its customers’ needs. While the retailer needs to deliver improved results quickly, we are unlikely to see any positive impact from changes made to the product proposition and target audience until the back end of 2018.

Alongside product, New Look’s store estate needs to be addressed. Its 596-strong UK store network, which has grown in the last two years despite clothing spend shifting from physical stores to online, is a huge encumbrance, and while closures will lead to market share loss in the short term, they are long awaited and necessary. A potential CVA would see New Look seek rent reductions across its store portfolio in addition to shuttering c.10% of its UK estate. We expect the closure of high rent, larger town centre stores to be prioritised in 2018, allowing it to benefit from greater cost savings in the short term. The retailer should also be closing stores in locations that have a younger demographic since online shopper penetration is higher, therefore its physical store shoppers are more likely to convert to its online channel.

In the longer term, its portfolio of outdated small format stores in local high street locations must also be rationalised as footfall levels continue to dwindle – making the size of its store estate more comparable to rivals H&M and Primark. These second and third tier stores carry a narrower product range and have little visual merchandising to draw in shoppers, so lack destination appeal and tarnish brand credibility. While New Look will have negotiated more attractive leases over the last five years as landlords work hard to maintain the presence of multiples, these stores will contribute little to group profitability and are expensive assets given the lack of investment they have received. A leaner store estate will improve space productivity, increase profit per store and provide a more consistent brand image.

New Look is set to release its Q3 results on 6 February, but with sales unlikely to have picked up over the Christmas period, the value retailer will find it hard to gain a positive momentum for what will be another tough year for high street clothing retailers. While New Look has a solid brand presence in the UK, it must build a strong leadership team under Alistair McGeorge, who led the company’s previous turnaround in 2011, to ensure drastic changes are implemented to enable the retailer’s survival.